Exemption in lieu of 80C tax benefits

In a bold move to simplify tax laws, the finance ministry is considering a plan to replace the tax benefits given to individuals for investing in specified savings instruments such as life insurance and provident funds with an upfront higher basic tax exemption limit.

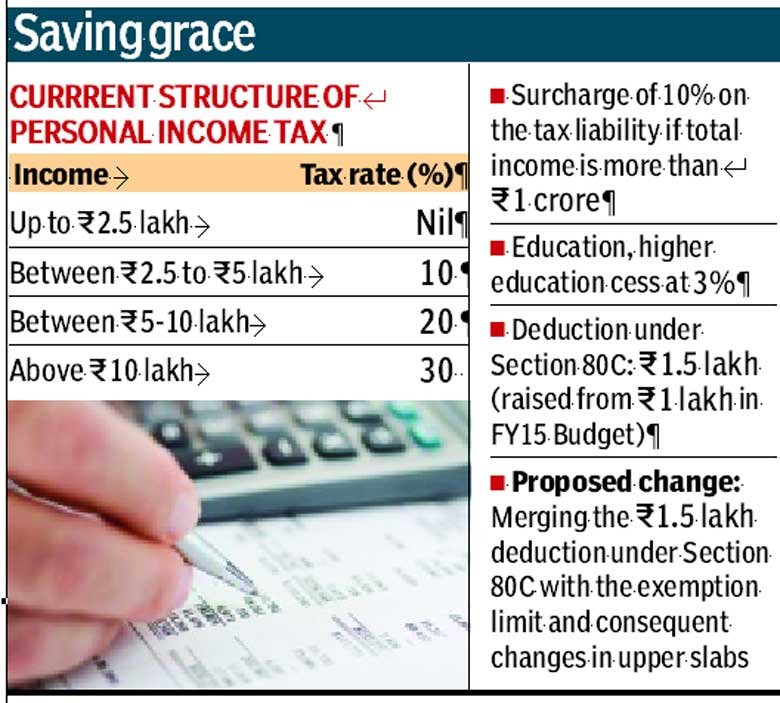

If the proposal makes it into Union Budget for 2015-16, the current R1.5 lakh deduction from the taxable income of individuals for investments in specified savings instruments under Section 80C of the Income Tax Act would be discontinued. Instead, the basic exemption limit would be correspondingly enhanced.

That is, individual’s income up to R4 lakh, or thereabouts, could be exempt from tax, up from Rs 2.5 lakh currently.

“Most of the complexities that exist in the Income Tax Act is on account of using tax policy as a tool for implementing certain genuine benefits and reliefs that the state wants to extend to taxpayers. These benefits could rather be given as upfront exemptions from taxation or outside the tax policy itself for the sake of simplicity,” explained a source privy to the discussions.

Also, the ministry reckons that the stated purpose of Section 80C, that is, to encourage household savings, is not efficiently achieved in the current model. It is practically difficult for the income tax department to verify that the investments are actually made by those seeking the deduction, especially those not covered under the tax-deduction-at-source (TDS) net.

As per the latest data, household financial savings stood at R12.8 lakh crore in 2013-14, accounting for 35% of the gross household savings of R20.65 lakh crore. Recent years saw household savings rate dipping.

“From a taxation perspective, its a good idea. However, the tax benefit given under Section 80C of the Income Tax Act has helped in boosting household savings. Certain instruments like the National Savings Certificate would not have seen investor appetite without this incentive,” said Neeru Ahuja, partner, Deloitte.

Sources, however, believe that the current system allows individuals to avail of the Section 80C benefit without having made the required investments.

Most of the tax returns by individuals are processed by what is called a ‘summary assessment’, under which an adjustment in the reported income is made only in cases of arithmetic error or of a wrong claim that is apparent from the return filed. Officials do not ask questions or insist on proof of investment while processing returns. Only in cases of ‘scrutiny assessment’ and ‘assessment of income that has earlier escaped assessment’, which are done in very few cases, more information or evidence is sought to ensure that the reported income is correct.

Even in the case of salaried individuals, where the employer may insist on proof of investments, the tax authorities do not. Besides, if a salaried individual wrongly claims in his return that Section 80C investments have been made, the TDS by the employer and paid to the department is refunded by the tax authorities without asking any questions. In the case of self-employed, there is no check either by the employer or the taxman.

So the ministry feels that any individual who is actually interested in saving would anyway do it and there is really no need to incentivise the same through the tax policy.

Savings entitled to tax benefit under Section 80C include payments towards life insurance, deferred annuity, provident funds, National Savings Certificates, unit-linked investment plans of LIC Mutual Fund, pension funds set up by mutual funds, equity-linked savings plans, deposits with National Housing Bank and tuition free paid for education of children.

Read more at:http://www.financialexpress.com/